This is the third in a series intended to help families better understand how to hold their School District spending student-centered and accountable.

By the time districts finalize their annual budgets, a large chunk of their total spending has already been decided. The clearest example of this is unallocated employee benefits which includes things like health insurance and pension contributions which are not optional and consistently rise.

This tracks across our 7-District Dashboard, with unallocated employee benefits having increased every year.

Through 2025, this category was one of the largest cost components outside of instruction and unlike textbooks or extracurriculars they don’t shift based on Board priorities or enrollment declines.

Despite its size, its’ also one of the easiest categories to miss on the ACFR precisely because it is labeled “unallocated”and doesn’t show up under instruction or administration.

Since folks tend to focus on instructional or departmental pages, benefit costs can appear invisible but when you look at it across multiple years, its behavior becomes unmistakable – a steady one directional trajectory regardless of what the rest of the budget ends up doing.

“Crowding Out”

Because most New Jersey districts operate under a 2% tax levy cap growth becomes a zero-sum game – a math problem created by policy. Even when you consider the exceptions for health benefits (which only kick in beyond the 2%), every extra dollar mandated for structural costs is a dollar the board can’t spend on a teacher or a student. Rising benefit costs swallow a margin that would otherwise be available for a new AP course or facility upgrade.And its not just that benefits are rising – they are “crowding out” the discretionary budget, potentially forcing boards to make cuts or stall improvements just to maintain the status quo.

Keep in mind we’re not looking at a static snapshot – costs compound annually, insurance premiums rise, pension obligations grow and formulas push the numbers upward. Even when districts hold the line on staffing or new programs – the unallocated benefits category will continue to expand.

BOEs have little ability to alter the trajectory in the short term since health benefits and pensions are governed by state rules, long-term agreements and statutory requirements.

Enrollment Mismatch and Legacy Costs

One of the most important dynamics the ACFR highlights is the interaction between benefit systems and enrollment trends. Many benefit obligations assume and are designed for stable or growing student populations.

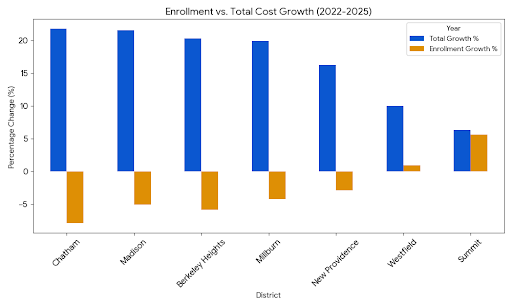

As I mentioned earlier, if enrollment declines the costs don’t go down with it. If a district loses 50 students across six grades they can’t just reduce staff or insurance groups which means that rising costs are spread across a smaller student pool. This creates a “scissors effect” where enrollment drops but the per-pupil cost surges.

The graph is a simple snapshot of this- in all but two Districts, enrollment has again declined yet total cost growth goes in the opposite direction.

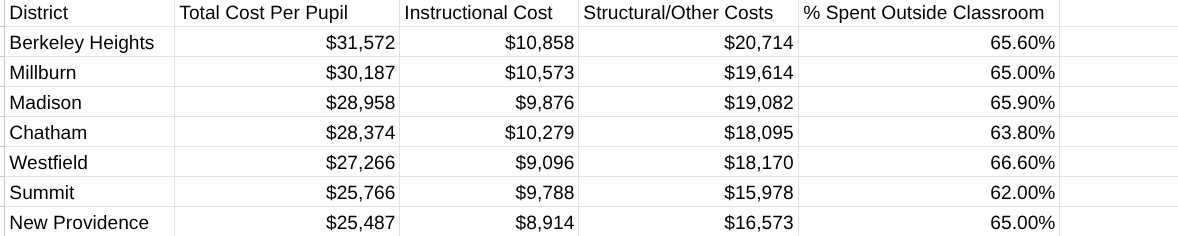

To understand this “Crowding Out” effect we can look at how much money actually reaches the classroom versus how much is consumed by structural obligations (benefits, facilities, debt, and other non-instructional costs).

Note: Other Costs includes unallocated benefits, operations, maintenance and debt service.

“Ghost in the Machine”

To understand the true scope of these costs, residents have to go past the headline budget numbers and into the ‘Notes to the Financial Statements’ where pension obligations and post-retirement health benefits are detailed. These rules require districts to report their share of state liabilities and while the district doesn’t “write the check” for the total liability today, these figures represent the underlying pressure that drives the annual premium increases you see in the budget.

Given that these costs are governed by realities created outside of local school districts, we haven’t given them a ton of attention in our discussions on school spending despite the price tag. Change on costs connected to unallocated benefits would require a lot of advocacy on the state level for that to happen.

Ultimately, the ACFR shows us that school districts aren’t just educational institutions but also massive insurance and pension cooperatives and that when we talk about the “cost of education,” we usually mean we’re discussing the “cost of employment.” Knowing where those costs exist and how they move over time is important if we’re to have any meaningful and honest conversation about school finances and long-term sustainability.

So, in our first article in the series, we saw that per-pupil costs are rising despite falling enrollment. In our second article we discovered that a good deal of money labeled ‘Instruction’ is often diverted to non-academic areas like Athletics. This article shows us one of the biggest cost factors (unallocated costs) are decided long before a school board even meets.

You can review the source documentation here.

Reference: DOE ACFR Page

Part of the NJ21st ACFR Series

This article is part of an ongoing NJ21st series using audited financial reports (ACFRs) to examine how school districts actually spend public dollars and what those choices mean for students.

View the full ACFR series →

|

Related Articles

Parking Hikes and Puppy Parks: The Rest of Summit’s Council Agenda

The 21st District Face-Off: How Seven Towns Stack Up on Per-Household Spending